![The First Step: Getting Pre-Approved for a Mortgage [INFOGRAPHIC] | Keeping Current Matters](https://files.keepingcurrentmatters.com/KeepingCurrentMatters/content/images/20240229/The-First-Step-Getting-Pre-Approved-for-a-Mortgage-KCM-Share.png)

What You Need to Know About the Mortgage Process [INFOGRAPHIC]

![What You Need to Know About the Mortgage Process [INFOGRAPHIC] | Simplifying The Market](http://files.simplifyingthemarket.com/wp-content/uploads/2018/07/17145720/20180720-Share-STM.jpg)

![What You Need to Know About the Mortgage Process [INFOGRAPHIC] | Simplifying The Market](http://files.simplifyingthemarket.com/wp-content/uploads/2018/07/17145659/Mortgage-Process-ENG-STM.jpg)

Some Highlights:

- Many buyers are purchasing a home with a down payment as little as 3%.

- You may already qualify for a loan, even if you don’t have perfect credit.

- Take advantage of the knowledge of your local professionals who are there to help you determine how much you can afford.

Powered by WPeMatico

Housing Will Not Fall Victim to Next Economic Storm

Some experts are calling for a slowdown in the economy later this year and most economists have predicted that the next recession could only be eighteen months away. The question is, what impact will a recession have on the housing market?

Here are the opinions of several experts on the subject:

Ivy Zelman in her latest “Z Report”:

“While economic activity appears to have accelerated so far in 2018, some prominent economic forecasters have become more cautious about growth prospects for 2019 and 2020…

All told, while solid long-term demographic underpinnings support our positive fundamental outlook for housing, in the event micro-economic headwinds surface, we would expect housing transaction volumes and home prices to weather the storm.”

Aaron Terrazas, Zillow’s Senior Economist:

“While much remains unknown about the precise path of the U.S. economy in the years ahead, another housing market crisis is unlikely to be a central protagonist in the next nationwide downturn.”

Mark Fleming, First American’s Chief Economist:

“If a recession is to occur, it is unlikely to be caused by housing-related activity, and therefore the housing sector should be one of the leading sources to come out of the recession.”

Mark J. Hulbert, Financial Analyst and Journalist:

“Real estate may be one of your best investments during the next bear market for stocks. And by real estate, I mean your home or other residential properties.”

U.S. News and World Report:

“Fortunately – and hopefully – the history of recessions and current issues that could harm the economy don’t lead many to believe the housing market crash will repeat itself in an upcoming decline.”

Powered by WPeMatico

Demand for Homes to Buy Continues to Climb

Across the United States, there is a severe mismatch between the low number of houses for sale and the high demand for those houses! First-time homebuyers are out in force and are being met with a highly competitive summer real estate market.

According to the National Association of Realtors (NAR), the inventory of homes for sale “has fallen year-over-year for 36 consecutive months,” and now stands at a 4.1-month supply. A 6-month supply of inventory is necessary for a balanced market and has not been seen since August of 2012.

NAR’s Chief Economist Lawrence Yun had this to say,

“Inventory coming onto the market during this year’s spring buying season – as evidenced again by last month’s weak reading – was not even close to being enough to satisfy demand.

That is why home prices keep outpacing incomes and listings are going under contract in less than a month – and much faster – in many parts of the country.”

Is There Any Relief Coming?

According to the CoreLogic’s 2018 Consumer Housing Sentiment Study, four times as many renters are considering buying homes in the next 12 months than homeowners who are planning to sell, “which is the crux of the available housing-supply imbalance.”

As more and more renters realize the benefits of homeownership, the demand for housing will continue to rise.

Do homeowners realize demand is so high? With home prices rising across the country, homeowners gained over a trillion dollars in equity over the last 12 months, with the average homeowner gaining over $16,000!

The map below shows the breakdown by state:

Many homeowners who have not thought about listing their homes may not even realize how much equity they have gained, or the opportunity available to them in today’s market!

Bottom Line

If you are one of the many homeowners across the country who hasn’t quite found their forever home, now may be a great time to list your house for sale and find your dream home!

Powered by WPeMatico

4 REAL Reasons Why We Buy A Home!

We often talk about why it makes financial sense to buy a home, but more often than not, the emotional reasons are the more powerful or compelling ones.

No matter what shape or size your living space is, the concept and feeling of home can mean different things to different people. Whether it’s a certain scent or a favorite chair, the emotional reasons why we choose to buy our own homes are typically more important to us than the financial ones.

1. Owning your home offers you the stability to start and raise a family

Between the best neighborhoods and the best school districts, even buyers without children at the time of purchase may have these things in mind as major reasons for choosing the locations of the homes that they purchase.

2. There’s no place like home

Owning your own home offers you not only safety and security, but also a comfortable place that allows you to relax after a long day!

3. You have more space for you and your family

Whether your family is expanding, an older family member is moving in, or you need to have a large backyard for your pets, you can take this all into consideration when buying your dream home!

4. You have control over renovations, updates, and style

Looking to actually try one of those complicated wall treatments that you saw on Pinterest? Tired of paying an additional pet deposit in your apartment building? Or maybe you want to finally adopt that puppy or kitten you’ve seen online 100 times? Who’s to say that you can’t do just that in your own home?

Bottom Line

Whether you are a first-time homebuyer or a move-up buyer who wants to start a new chapter in your life, now is a great time to reflect on the intangible factors that make a house a home.

Powered by WPeMatico

First-Time Home Buyers Continue to Put Down Less Than 6%!

According to the Realtors Confidence Index from the National Association of Realtors, 61% of first-time homebuyers purchased their homes with down payments below 6% in 2017.

Many potential homebuyers believe that a 20% down payment is necessary to buy a home and have disqualified themselves without even trying, but in March, 71% of first-time buyers and 54% of all buyers put less than 20% down.

Ralph McLaughlin, Chief Economist and Founder of Veritas Urbis Economics, recently shed light on why buyer demand has remained strong,

“The fact that we now have four consecutive quarters where owner households increased while renters households fell is a strong sign households are making the switch from renting to buying.

Households under 35 – which represent the largest potential pool of new homeowners in the U.S. – have shown some of the largest gains. While they only make up a third of all homebuyers, the steady uptick in their homeownership rate over the past year suggests their enormous purchasing power may be finally coming to [the] housing market.”

It’s no surprise that with rents rising, more and more first-time buyers are taking advantage of low-down-payment mortgage options to secure their monthly housing costs and finally attain their dream homes.

Bottom Line

If you are one of the many first-time buyers unsure of whether or not they would qualify for a low-down payment mortgage, let’s get together and set you on your path to homeownership!

Powered by WPeMatico

Want to Sell Your House Faster? Don’t Forget to Stage! [INFOGRAPHIC]

![Want to Sell Your House Faster? Don’t Forget to Stage! [INFOGRAPHIC] | Simplifying The Market](http://files.simplifyingthemarket.com/wp-content/uploads/2018/07/11165628/20180713-STM-ENG.jpg)

Some Highlights:

- The National Association of Realtors surveyed their members & released the findings of their Profile of Home Staging.

- 62% of seller’s agents say that staging a home decreases the amount of time a home spends on the market.

- 50% of staged homes saw a 1-10% increase in dollar-value offers from buyers.

- 77% of buyer’s agents said staging made it easier for buyers to visualize the home as their own.

- The top rooms to stage in order to attract more buyers are the living room, master bedroom, kitchen, and dining room.

Powered by WPeMatico

House-Buying Power at Near-Historic Levels

We keep hearing that home affordability is approaching crisis levels. While this may be true in a few metros across the country, housing affordability is not a challenge in the clear majority of the country. In their most recent Real House Price Index, First American reported that consumer “house-buying power” is at “near-historic levels.”

Their index is based on three components:

- Median Household Income

- Mortgage Interest Rates

- Home Prices

The report explains:

“Changing incomes and interest rates either increase or decrease consumer house-buying power or affordability. When incomes rise and/or mortgage rates fall, consumer house-buying power increases.”

Combining these three crucial pieces of the home purchasing process, First American created an index delineating the actual home-buying power that consumers have had dating back to 1991.

Here is a graph comparing First American’s consumer house-buying power (blue area) to the actual median home price that year from the National Association of Realtors (yellow line).

Consumer house-buyer power has been greater than the actual price of a home since 1991. And, the spread is larger over the last decade.

Bottom Line

Even though home prices are increasing rapidly and are now close to the values last seen a decade ago, the actual affordability of a home is much better now. As Chief Economist Mark Fleming explains in the report:

“Though unadjusted house prices have risen to record highs, consumer house-buying power stands at near-historic levels, as well, signaling that real house prices are not even close to their historical peak.”

Powered by WPeMatico

Rising Interest Rates Have Not Dampened Demand

Since the beginning of the year, mortgage interest rates have risen over a half of a percentage point (from 3.95% to 4.52%), according to Freddie Mac. Even a small rise in interest rates can greatly impact a buyer’s monthly mortgage payment.

First American recently released the results of their quarterly Real Estate Sentiment Index (RESI), in which they surveyed title and real estate agents across the country about the impact of rising rates on first-time homebuyers.

Real estate professionals around the country have not noticed a slowdown in demand for housing among young buyers; nearly 93% of all first-time homebuyers last quarter were between the ages of 21-35, with the largest share of buyers (51%) coming from those ages 26-30.

First American’s Chief Economist Mark Fleming had this to say,

“On a national level, mortgage rates would need to hit 5.6%, 1 percentage point above the current rate, before first-time homebuyers withdraw from the market.”

So, what is slowing down sales?

According to the last Existing Home Sales Report from the National Association of Realtors, sales are now down 3.0% year-over-year and have fallen for the last three months. If rising interest rates aren’t to blame, then what is?

Fleming addressed the cause, saying that:

“The housing market is facing its greatest supply shortage in 60 years of record keeping, according to the Federal Reserve Bank of Kansas City. The ongoing housing supply shortage will make it difficult for first-time buyers to find a home to buy, even when they are financially ready.”

Bottom Line

First-time homebuyers know the importance of owning their own homes and a spike in interest rates is not going to keep them from buying this year! Their biggest challenge is finding a home to buy!

Powered by WPeMatico

How Long Do Most Families Live in a House?

The National Association of Realtors (NAR) keeps historical data on many aspects of homeownership. One of their data points, which has changed dramatically, is the median tenure of a family in a home, meaning how long a family stays in a home prior to moving.

As the graph below shows, over the last twenty years (1985-2008), the median tenure averaged exactly six years. However, since 2014, that average is almost ten years – an increase of almost 50%.

Why the dramatic increase?

The reasons for this change are plentiful!

The fall in home prices during the housing crisis left many homeowners in a negative equity situation (where their home was worth less than the mortgage on the property). Also, the uncertainty of the economy made some homeowners much more fiscally conservative about making a move.

With home prices rising dramatically over the last several years, 95.3% of homes with a mortgage are now in a positive equity situation, according to CoreLogic.

With the economy coming back and wages starting to increase, many homeowners are in a much better financial situation than they were just a few short years ago.

One other reason for the increase was brought to light by NAR in their 2018 Home Buyer and Seller Generational Trends Report. According to the report,

“Sellers 37 years and younger stayed in their home for six years…”

These homeowners, who are either looking for more space to accommodate their growing families or for better school districts to do the same, are likely to move more often (compared to typical sellers who stayed in their homes for 10 years). The homeownership rate among young families, however, has still not caught up to previous generations, resulting in the jump we have seen in median tenure!

What does this mean for housing?

Many believe that a large portion of homeowners are not in a house that is best for their current family circumstance; they could be baby boomers living in an empty, four-bedroom colonial, or a millennial couple living in a one-bedroom condo planning to start a family.

These homeowners are ready to make a move, and since a lack of housing inventory is still a major challenge in the current housing market, this could be great news.

Powered by WPeMatico

The #1 Reason to List Your House for Sale NOW!

If you are debating whether or not to list your house for sale this year, here is the #1 reason not to wait!

Buyer Demand Continues to Outpace the Supply of Homes for Sale

The National Association of Realtors’ (NAR) Chief Economist Lawrence Yun recently commented on the current lack of inventory:

“Inventory coming onto the market during this year’s spring buying season – as evidenced again by last month’s weak reading – was not even close to being enough to satisfy demand.

That is why home prices keep outpacing incomes and listings are going under contract in less than a month – and much faster – in many parts of the country.”

The latest Existing Home Sales Report shows that there is currently a 4.1-month supply of homes for sale. This remains lower than the 6-month supply necessary for a normal market, and 6.1% lower than last year’s inventory level.

The chart below details the year-over-year inventory shortages experienced over the last 12 months:

Anything less than a six-month supply is considered a “seller’s market.”

Bottom Line

Let’s get together to discuss the supply conditions in our neighborhood so that I can assist you in gaining access to the buyers who are ready, willing, and able to buy right now!

Powered by WPeMatico

Cost Across Time [INFOGRAPHIC]

![Cost Across Time [INFOGRAPHIC] | Simplifying The Market](http://files.simplifyingthemarket.com/wp-content/uploads/2018/07/03135850/20180706-Share-STM.jpg)

![Cost Across Time [INFOGRAPHIC] | Simplifying The Market](http://files.simplifyingthemarket.com/wp-content/uploads/2018/07/03135755/20180706-STM-ENG.jpg)

Some Highlights:

- With interest rates still around 4.5%, now is a great time to look back at where rates have been over the last 40 years.

- Rates are projected to climb to 5.1% by this time next year according to Freddie Mac.

- The impact your interest rate makes on your monthly mortgage cost is significant!

- Lock in a low rate now while you can!

Powered by WPeMatico

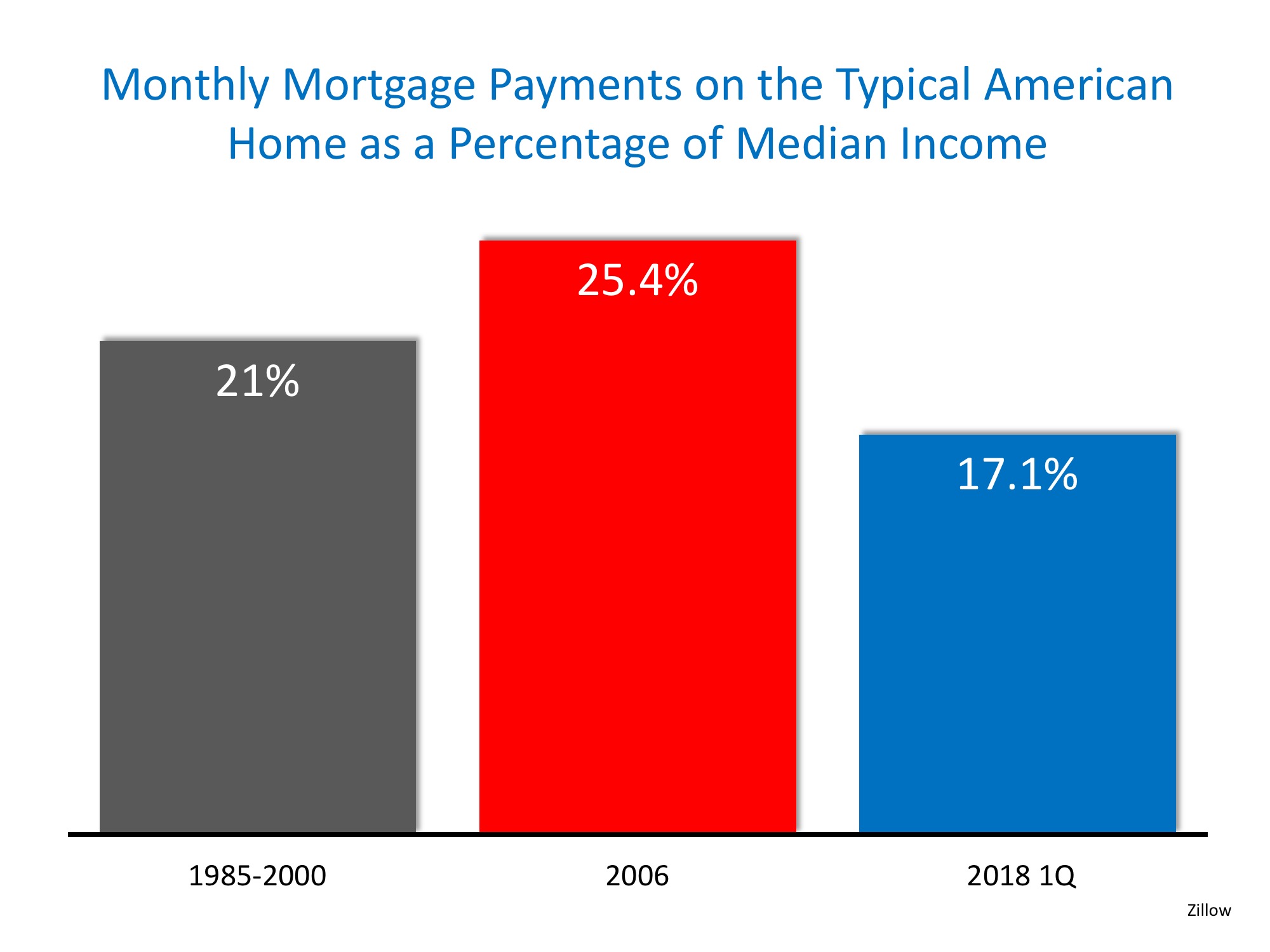

Homes More Affordable Today than 1985-2000

Rising home prices have many concerned that the average family will no longer be able to afford the most precious piece of the American Dream – their own home.

However, it is not just the price of a home that determines its affordability. The monthly cost of a home is determined by the price and the interest rate on the mortgage used to purchase it.

Today, mortgage interest rates stand at about 4.5%. The average annual mortgage interest rate from 1985 to 2000 was almost double that number, at 8.92%. When comparing affordability of homeownership over the decades, we must also realize that incomes have increased.

This is why most indexes use the percentage of median income required to make monthly mortgage payments on a typical home as the point of comparison.

Zillow recently released a report comparing home affordability over the decades using this formula. The report revealed that, though homes are less affordable this year than last year, they are more affordable today (17.1%) than they were between 1985-2000 (21%). Additionally, homes are more affordable now than at the peak of the housing bubble in 2006 (25.4%). Here is a chart of these findings:

What will happen when mortgage interest rates rise?

Most experts think that the mortgage interest rate will increase to about 5% by year’s end. How will that impact affordability? Zillow also covered this in their report:

Rates would need to approach 6% before homes became less affordable than they had been historically.

Bottom Line

Though homes are less affordable today than they were last year, they are still a great purchase while interest rates are below the 6% mark.

Powered by WPeMatico

VA Loans: Making a Home for the Brave Possible

Since the creation of the Veterans Affairs (VA) Home Loans Program, over 22 million veterans have achieved the American Dream of homeownership. Many veterans do not know the details of the program and therefore do not take advantage of the benefits available to them.

If you are a veteran or you know someone who is, here is a breakdown of the VA Home Loan benefits that can be used to achieve the American Dream!

Top 5 Benefits of a VA Home Loan

- The greatest benefit of a VA Loan is that borrowers can buy a home with a 0% down payment. In 2016, 82% of all VA Loans put down 0%!

- Primary Mortgage Insurance (PMI) is not required! (Most other loans with down payments under 20% require PMI, which adds additional costs to your monthly housing expense!)

- Credit Score requirements are also lower for VA Home Loans. The average FICO® score of a borrower for an approved VA Loan is 620, compared to 676 (FHA) or 753 (Conventional).

- There is also a limitation on a veteran buyer’s closing costs. Sellers can pay all of a buyer’s loan-related closing costs and up to 4% in concessions in some cases.

- Even with interest rates rising, VA Loans continue to have the lowest average interest rates of all loan types.

Who Qualifies for a VA Home Loan?

One of the most important first steps when applying for a VA Home Loan is obtaining your Certificate of Eligibility (COE). “The COE verifies to the lender that you are eligible for a VA-backed loan.”

You Can Apply for a VA Loan if You:

- Serve 90 consecutive days during wartime

- Serve 181 consecutive days during peacetime

- Have more than 6 years in the National Guard or Reserves

- Are the spouse of a service member who has died in the line of duty or as the result of a service-related disability

You Can Use a VA Loan To:

- Purchase a Home

- Purchase a Condo

- Build a Home

- Refinance an existing home loan

- Make improvements to a home by installing energy-related features or making energy-efficient improvements

Bottom Line

For more information or to find out if you or a loved one would qualify to use the VA Home Loan Benefit, let’s get together! Thank you for your service!

Powered by WPeMatico

Why Should You Use A Professional to Sell Your Home?

When homeowners decide to sell their houses, they obviously want to get the best possible price for their home with the least amount of hassles along the way. However, for the vast majority of sellers, the most important result is actually getting their homes sold.

In order to accomplish all three goals, a seller should realize the importance of using a real estate professional. We realize that technology has changed a buyer’s behavior during the home buying process. According to the National Association of Realtors’ 2018 Home Buyer & Seller Generational Trends Report, the first step that “42% of recent buyers took in the home buying process was to look online at properties for sale.”

However, the report also revealed that 94% of buyers who used the internet when searching for homes ultimately purchased their homes through either a real estate agent/broker or from a builder or builder’s agent. Only 2% of buyers purchased their homes directly from a seller whom they didn’t know.

Buyers search for a home online but then depend on an agent to find the home they will buy (52%), to negotiate the terms of the sale (47%) & price (38%), or to help understand the process (60%).

The plethora of information now available has resulted in an increase in the percentage of buyers who reach out to real estate professionals to “connect the dots.” This is obvious, as the percentage of overall buyers who have used agents to buy their homes has steadily increased from 69% in 2001.

Bottom Line

If you are thinking of selling your home, don’t underestimate the role a real estate professional can play in the process.

Powered by WPeMatico

Buying This Summer? Be Prepared for Bidding Wars

Summer is traditionally a busy season for real estate. Buyers come out in force and homeowners list their houses for sale hoping to capitalize on those buyers who are looking to purchase before the new school year. This year will be no different!

Buyers have already been out in force looking for their dream homes and more are on their way. The challenge is that the inventory of homes for sale has not kept up with demand, which has led to A LOT of competition for the homes that are available.

A recent article by the National Association of Realtors touched on the current market conditions:

“Realtors® in areas with strong job markets report that consumer frustration is rising. Home shoppers are increasingly struggling to find an affordable property to buy, and the prevalence of multiple bids is pushing prices further out of reach.”

Realtor.com went on to explain why buyers are flocking to the market in such big numbers:

“A booming economy and stable employment in most parts of the country have created a new generation of eager home buyers – and led to fevered price battles spilling over into some unexpected, smaller markets.”

Javier Vivas, Director of Economic Research for Realtor.com had this to say about competition:

“Multiple-offer scenarios are no longer reserved to the usual big, fast-moving markets…demand for homes has spilled outward into secondary, smaller markets, and more buyers are gearing up to face fierce competition in more places around the country.”

Realtor.com looked at the number of homes that were selling above asking price to determine which markets were heating up. Below are the Top 10:

- Akron, OH

- Worcester, MA

- Lexington, KY

- Irvine, CA

- Greensboro, NC

- Sioux Falls, SD

- Madison, WI

- Louisville, KY

- Tacoma, WA

- Little Rock, AR

Bottom Line

Let’s get together to discuss our exact market conditions so that we can help you create a strategy to secure your new home in this competitive atmosphere!

Powered by WPeMatico

5 Reasons Millennials Choose to Buy a Home [INFOGRAPHIC]

![5 Reasons Millennials Choose to Buy a Home [INFOGRAPHIC] | Simplifying The Market](http://files.simplifyingthemarket.com/wp-content/uploads/2018/06/26162117/20180629-STM-ENG.jpg)

Some Highlights:

- “The majority of millennials said they consider owning a home more sensible than renting for both financial and lifestyle reasons — including control of living space, flexibility in future decisions, privacy and security, and living in a nice home.”

- The top reason millennials choose to buy is to have control over their living space, at 93%.

- Many millennials who rent a home or apartment prior to buying their own homes dream of the day when they will be able to paint the walls whatever color they’d like or renovate an outdated part of their living space.

Powered by WPeMatico

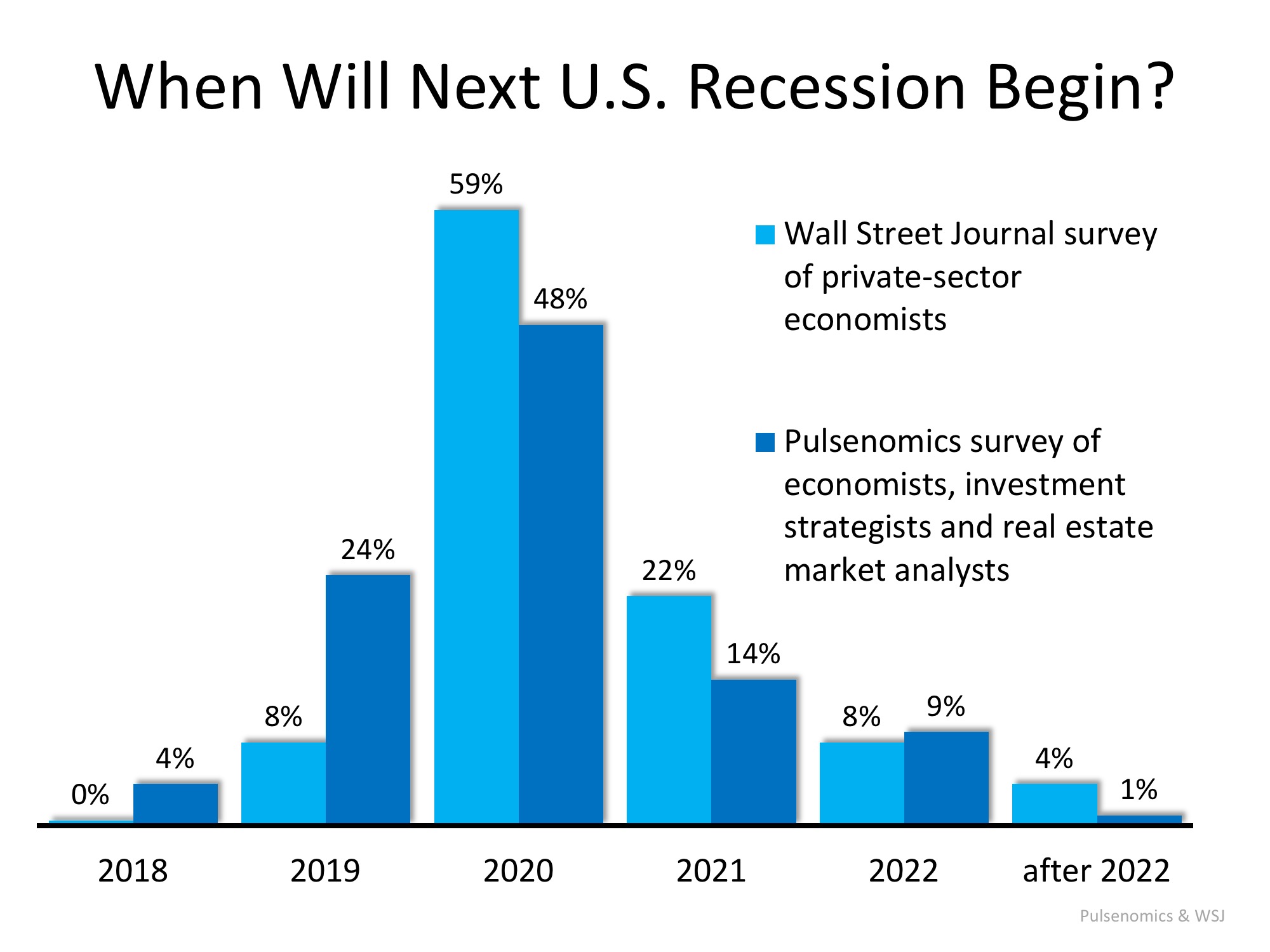

Next Recession in 2020? What Will Be the Impact?

Economists and analysts know that the country has experienced economic growth for almost a decade. They also know that a recession can’t be too far off. A recent report by Zillow Research shed light on a survey conducted by Pulsenomics in which they asked economists, investment strategists and market analysts how they felt about the current housing market. That report revealed the possible timing of the next recession:

“Experts largely expect the next recession to begin in 2020.”

That timing concurs with a recent survey of economists by the Wall Street Journal:

“The economic expansion that began in mid-2009 and already ranks as the second-longest in American history most likely will end in 2020 as the Federal Reserve raises interest rates to cool off an overheating economy, according to forecasters surveyed.”

Here is a graph comparing the opinions of those surveyed by both the Wall Street Journal and Pulsenomics:

Recession DOES NOT Equal Housing Crisis

According to the Merriam-Webster Dictionary, a recession is defined as follows:

“A period of temporary economic decline during which trade and industrial activity are reduced, generally identified by a fall in GDP in two successive quarters.”

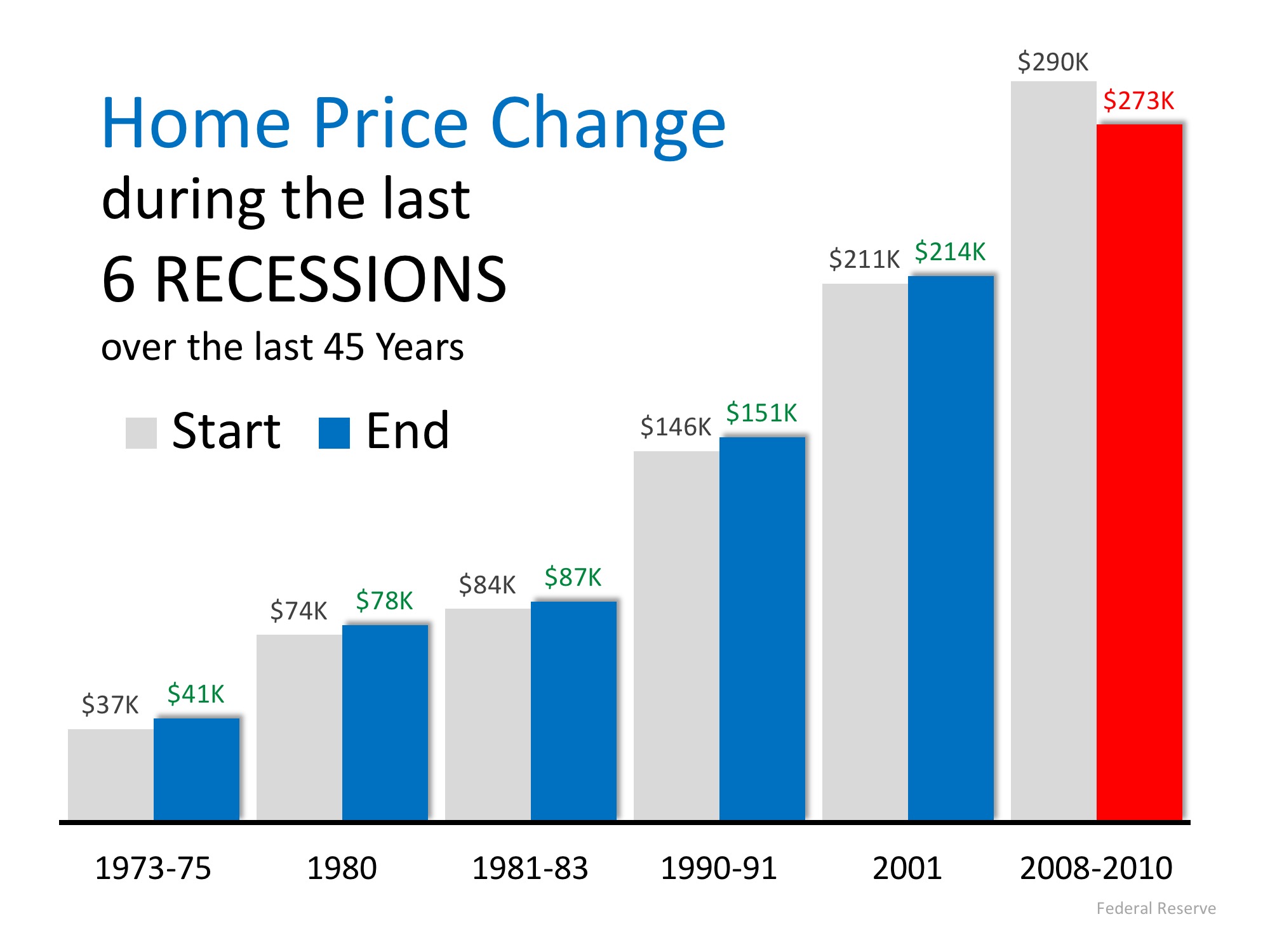

A recession means the economy has slowed down markedly. It does not mean we are experiencing another housing crisis. Obviously, the housing crash of 2008 caused the last recession. However, during the previous five recessions home values appreciated.

According to the experts surveyed by Pulsenomics, the top three probable triggers for the next recession are:

- Monetary policy

- Trade policy

- A stock market correction

A housing market correction was ranked ninth in probability. Those same experts also projected that home values would continue to appreciate in 2019, 2020, 2021 and 2022.

Others agree that housing will not be impacted like it was a decade ago.

Mark Fleming, First American’s Chief Economist, explained:

“If a recession is to occur, it is unlikely to be caused by housing-related activity, and therefore the housing sector should be one of the leading sources to come out of the recession.”

And U.S. News and World Report agreed:

“Fortunately – and hopefully – the history of recessions and current issues that could harm the economy don’t lead many to believe the housing market crash will repeat itself in an upcoming decline.”

Bottom Line

A recession is probably less than two years away. A housing crisis is not.

Powered by WPeMatico

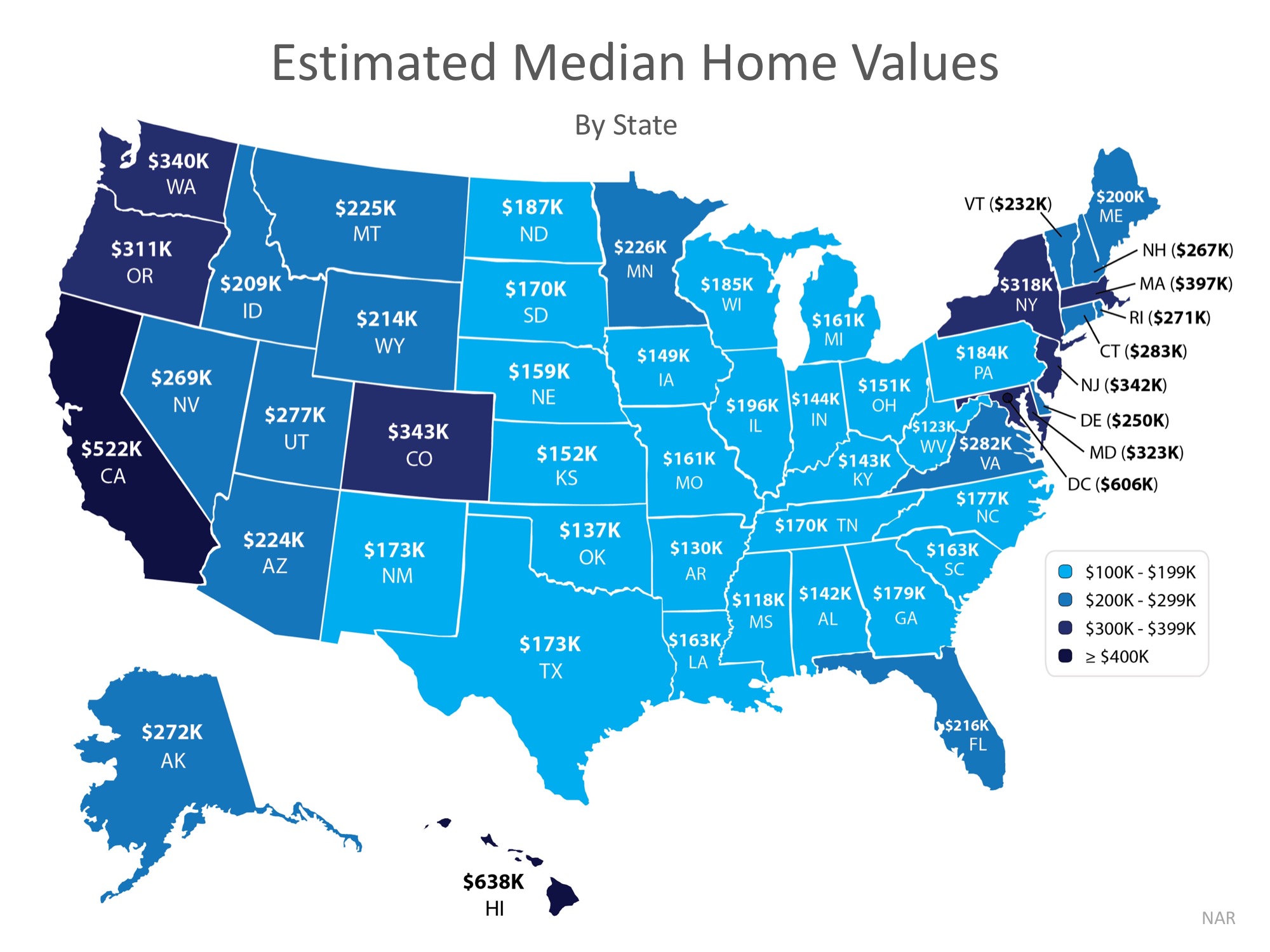

What’s the Median Home Value in Your State?

If you’ve entered the real estate market as a buyer or a seller, you’ve inevitably heard the mantra “location, location, location” in reference to identical homes increasing or decreasing in value based on where they’re located.

In today’s housing market where home prices are appreciating quickly, it’s important to know that not every home appreciates at the same rate. The map below demonstrates that point on a state-by-state basis using data from the National Association of Realtors.

Demand often dictates value, even for houses in the same area of the country! High demand for starter and trade-up homes have driven prices up in these categories by nearly 10% over the past year, while those in the premium markets have appreciated at closer to 6%.

Bottom Line

If you are debating whether or not to buy and/or sell a home this year, let’s get together to help you figure out exactly what’s going on in our market.

Powered by WPeMatico

Are You Wondering If You Can Buy Your First Home?

There are many people sitting on the sidelines trying to decide if they should purchase a home or sign a rental lease. Some might wonder if it makes sense to purchase a house before they get married or start a family, some might think they are too young, and still, some others might think their current incomes would never enable them to qualify for a mortgage.

We want to share what the typical first-time homebuyer actually looks like based on the National Association of Realtors’ most recent Profile of Home Buyers & Sellers. Here are some interesting revelations on the first-time buyer:

Bottom Line

You may not be much different than many people who have already purchased their first homes. Let’s meet to determine if your dream home is within your grasp today.

Powered by WPeMatico

You DO NOT Need 20% Down to Buy Your Home NOW!

The Aspiring Home Buyers Profile from the National Association of Realtors (NAR) found that the American public is still somewhat confused about what is required to qualify for a home mortgage loan in today’s housing market. The results of the survey show that the main reason why non-homeowners do not own their own homes is because they believe that they cannot afford them.

This brings us to two major misconceptions that we want to address today.

1. Down Payment

A recent survey by Laurel Road, the National Online Lender and FDIC-Insured Bank, revealed that consumers overestimate the down payment funds needed to qualify for a home loan.

According to the survey, 53% of Americans who plan to buy or have already bought a home admit to their concerns about their ability to afford a home in the current market. In addition, 46% are currently unfamiliar with alternative down payment options, and 46% of millennials do not feel confident that they could currently afford a 20% down payment.

What these people don’t realize, however, is that there are many loans written with down payments of 3% or less.

Many renters may actually be able to enter the housing market sooner than they ever imagined with new programs that have emerged allowing less cash out of pocket.

2. FICO®Scores

An Ipsos survey revealed that 62% of respondents believe they need excellent credit to buy a home, with 43% thinking a “good credit score” is over 780. In actuality, the average FICO® scores for approved conventional and FHA mortgages are much lower.

The average conventional loan closed in May had a credit score of 753, while FHA mortgages closed with an average score of 676. The average across all loans closed in May was 724. The chart below shows the distribution of FICO® Scores for all loans approved in May.

Bottom Line

If you are a prospective buyer who is ‘ready’ and ‘willing’ to act now, but you are not sure if you are ‘able’ to, let’s sit down to help you understand your true options today.

Powered by WPeMatico

4 Reasons to Sell This Summer [INFOGRAPHIC]

![4 Reasons to Sell This Summer [INFOGRAPHIC] | Simplifying The Market](http://files.simplifyingthemarket.com/wp-content/uploads/2018/06/21133003/4-Reasons-To-Sell-Summer-ENG-STM.jpg)

Some Highlights:

- Buyer demand continues to outpace the supply of homes for sale which means that buyers are often competing with one another for the few listings that are available!

- Housing inventory is still under the 6-month supply needed to sustain a normal housing market.

- Perhaps the time has come for you and your family to move on and start living the life you desire.

Powered by WPeMatico

Homes are More Affordable in 44 out of 50 States

With both home prices and mortgage rates increasing this year, many are concerned about a family’s ability to purchase a major part of the American Dream – its own home. However, if we compare housing affordability today to the average affordability prior to the housing boom and bust, we are in much better shape than most believe.

In Black Knight’s latest monthly Mortgage Monitor, they revealed that in the vast majority of the country, it is actually more affordable to purchase a home today than it was between 1995 to 2003 when looking at mortgage payments (determined by price and interest rate) as compared to incomes. Home prices are up compared to 1995-2003, but mortgage rates are still much lower now than at that time. Today, they stand at about 4.5%. Here are the average mortgage rates for each of the years mentioned:

- 1995 – 7.93%

- 1996 – 7.81%

- 1997 – 7.6%

- 1998 – 6.94%

- 1999 – 7.44%

- 2000 – 8.05%

- 2001 – 6.97%

- 2002 – 6.54%

- 2003 – 5.83%

On the other hand, wages have risen over the last twenty years.

Black Knight’s research revealed that, when comparing “the share of median income required to buy the median-priced home” today, to the average between 1995 to 2003, it is currently more affordable to purchase a home in 44 of 50 states.

Here is a state map of the percentage change in the price-to-payment ratio. Positive numbers indicate that it is less affordable to buy while negative numbers indicate that it is more affordable.

Bottom Line

Whether you are moving up to the home of your dreams or purchasing your first house, it is a great time to buy when looking at historic affordability data.

Powered by WPeMatico