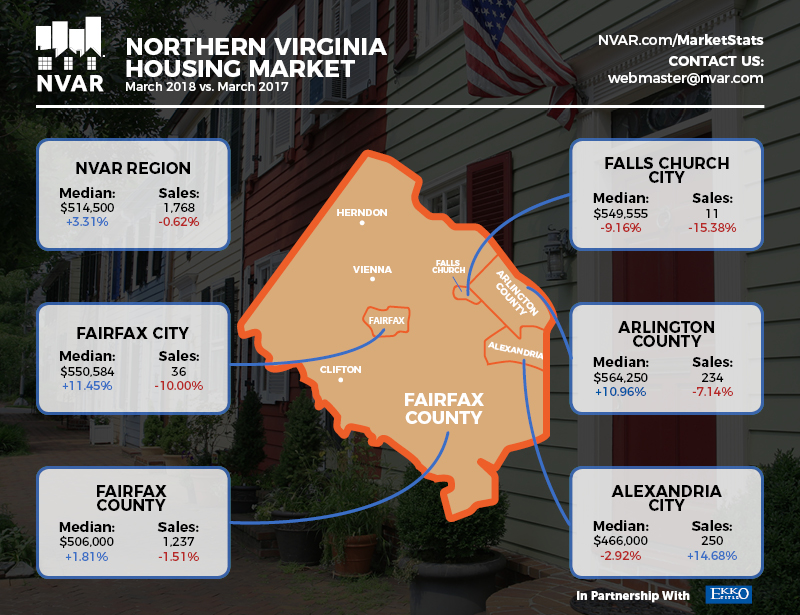

The Northern Virginia Association of Realtors® reports on March 2018 home sales activity for Fairfax and Arlington counties, the cities of Alexandria, Fairfax and Falls Church and the towns of Vienna, Herndon and Clifton.

According to the Northern Virginia Association of Realtors, March 2018 continued the trend of tight supply of homes for sale, and stiff competition for the available homes. Buyers in the starter home market are particular impacted, because bidding wars often shut out buyers that have more modest means.

Year over year totals of home sold were off less than 1%. March 2018 saw a total of 1,768 homes sold, compared to 1,779 homes sold in March 2017.

Market uncertainty and rising interest rates may be causing some sellers to stay on the sidelines. Active listings decreased in March 2018 when compared with March 2017 — down about 21 percent below last year, with 2,891 active listings in March, compared with 3,667 homes available in March 2017.

Demonstrated continued strong demand, despite lack of available homes, the average days on market (DOM) for was 42 days in March 2018, compared to the 52 DOM for homes in March 2017. This is a a decrease of about 19 percent.

The average home sale price remains comparatively flat year over year. March 2018 reflects average prices at $568,576, up by barely 1 percent compared to a year prior, with an average price of $565,964.

The median sold price was $514,500 for homes sold in March 2018, which is an increase of 3.31 percent compared to the median price of $498,000 in March 2017.

As expected when fewer homes are available on the market, pending home sales in Northern Virginia in March 2018 were 7.25 percent below March of last year. Total pending sales were off by 10.72 percent compared with the pending contracts in March 2017.

While the markets pose some challenges, for those who have been saving and preparing for a new home purchase can still find opportunities. As interest rates and prices are expected to continue to rise, waiting could cost you money in the long run.

Herbert Riggs and Associates can help you with all your real estate needs. Whether buying, selling, or investing, If you have any questions, give me a call at 703-966-2647 or send me an email at Herbert.Riggs@gmail.com.

Read more

![Existing Home Sales Grow Despite Low Inventory [INFOGRAPHIC] | Simplifying the Market](http://files.simplifyingthemarket.com/wp-content/uploads/2018/04/24163655/20180427-Share-STM.jpg)

![Existing Home Sales Grow Despite Low Inventory [INFOGRAPHIC] | Simplifying the Market](http://files.simplifyingthemarket.com/wp-content/uploads/2018/04/24163629/20180427-EHS-Report-STM-ENG.jpg)

![A Tale of Two Markets [INFOGRAPHIC] | Simplifying The Market](http://files.simplifyingthemarket.com/wp-content/uploads/2018/04/12175652/Two-Markets-STM-ENG.jpg)

![VA Loans by the Numbers [INFOGRAPHIC] | Simplifying The Market](http://files.simplifyingthemarket.com/wp-content/uploads/2018/04/05165336/20180506-STM-ENG.jpg)

![The Cost of Renting vs. Buying Today [INFOGRAPHIC] | Simplifying The Market](http://files.simplifyingthemarket.com/wp-content/uploads/2018/03/27150933/Rent-vs.-Buy-STM.jpg)